1. Introduction

In this post I work through the main results in Ang, Hodrick, Xing, and Zhang (2006) which shows not only that i) stocks with more exposure to changes in aggregate volatility have higher average excess returns, but also that ii) stocks with more idiosyncractic volatility relative to the Fama and French (1993)  factor model have lower excess returns. The first result is consistent with existing asset pricing theories; whereas, the second result is at odds with almost any mainstream asset pricing theory you might write down. Idiosyncratic risk should not be priced. This paper together with Campbell, Lettau, Malkiel, and Xu (2001) (see my earlier post) set off an investigation into the role of idiosyncratic risk in determining asset prices. One possibility is that idiosyncratic risk is just a proxy for exposure to aggregate risk. i.e., perhaps it’s the firms with the highest exposure to aggregate return volatility that also have the highest idiosyncratic volatility. Interestingly, Ang, Hodrick, Xing, and Zhang (2006) show that this is not the case via a double sort on both aggregate and idiosyncratic volatility exposure giving evidence that these are

factor model have lower excess returns. The first result is consistent with existing asset pricing theories; whereas, the second result is at odds with almost any mainstream asset pricing theory you might write down. Idiosyncratic risk should not be priced. This paper together with Campbell, Lettau, Malkiel, and Xu (2001) (see my earlier post) set off an investigation into the role of idiosyncratic risk in determining asset prices. One possibility is that idiosyncratic risk is just a proxy for exposure to aggregate risk. i.e., perhaps it’s the firms with the highest exposure to aggregate return volatility that also have the highest idiosyncratic volatility. Interestingly, Ang, Hodrick, Xing, and Zhang (2006) show that this is not the case via a double sort on both aggregate and idiosyncratic volatility exposure giving evidence that these are  separate risk factors. The code I use to replicate the results in Ang, Hodrick, Xing, and Zhang (2006) and create the figures can be found here.

separate risk factors. The code I use to replicate the results in Ang, Hodrick, Xing, and Zhang (2006) and create the figures can be found here.

2. Theoretical Motivation

The discount factor view of asset pricing says that:

(1) ![\begin{align*} 0 = \mathrm{E}[m \cdot r_n] \quad \text{for all } n=1,2,\ldots,N \end{align*}](https://alexchinco.com/wp-content/ql-cache/quicklatex.com-508a9b2be9012405afbe52f1f9ace924_l3.svg "Rendered by QuickLaTeX.com")

where  denotes the expectation operator,

denotes the expectation operator,  denotes the stochastic discount factor, and

denotes the stochastic discount factor, and  denotes asset

denotes asset  ‘s excess return. Equation (1) reads: “In the absence of margin requirements and transactions costs, it costs you

‘s excess return. Equation (1) reads: “In the absence of margin requirements and transactions costs, it costs you  today to borrow at the riskless rate, buy a stock, and hold the position for

today to borrow at the riskless rate, buy a stock, and hold the position for  period.” Asset pricing theories explain why average excess returns,

period.” Asset pricing theories explain why average excess returns, ![\mathrm{E}[r_n]](https://alexchinco.com/wp-content/ql-cache/quicklatex.com-c1c4d3c62fc95adb501bdfff487e1cc8_l3.svg "Rendered by QuickLaTeX.com") , vary across assets even though they all have the same price today by construction (see my earlier post).

, vary across assets even though they all have the same price today by construction (see my earlier post).

Suppose each asset’s excess returns are a function of a risk factor  ,

,  , and noise,

, and noise,  :

:

(2)

where I assume for simplicity that the only risk factor is the value-weighted excess return on the market so that  and

and  . I use a Taylor expansion to linearize the function around the point

. I use a Taylor expansion to linearize the function around the point  and assume

and assume  terms are negligible so

terms are negligible so ![\mathrm{E}[r_n] = \alpha_n + \sfrac{\gamma_n}{2} \cdot \sigma_x^2](https://alexchinco.com/wp-content/ql-cache/quicklatex.com-9a3e91c7bd5a49c76324b127fc7bd134_l3.svg "Rendered by QuickLaTeX.com") and

and ![\mathrm{Var}[r_n] = \beta_n^2 \cdot \sigma_x^2 + \sigma_z^2](https://alexchinco.com/wp-content/ql-cache/quicklatex.com-12e2da3ed43e012d1ce11a6f7a4afbad_l3.svg "Rendered by QuickLaTeX.com") . This means that if the excess return on the market is

. This means that if the excess return on the market is  larger than expected, then asset ‘s expected excess returns will be

larger than expected, then asset ‘s expected excess returns will be  larger.

larger.

Any asset pricing theory says that each asset’s expected excess return should be proportional to how much the asset comoves with the risk factor, :

(3) ![\begin{align*} \mathrm{E}[r_n] = \alpha_n + \frac{\gamma_n}{2} \cdot \sigma_x^2 = \underbrace{\text{Constant} \times \beta_n}_{\text{Predicted}} \end{align*}](https://alexchinco.com/wp-content/ql-cache/quicklatex.com-b39998197ded6695fa456331032ccb3b_l3.svg "Rendered by QuickLaTeX.com")

where the constant of proportionality, ![\text{Constant} = c \cdot (\sfrac{\mathrm{Var}[m]}{\mathrm{E}[m]})](https://alexchinco.com/wp-content/ql-cache/quicklatex.com-f0e508f53a2eab3a7440848bea6904b4_l3.svg "Rendered by QuickLaTeX.com") , depends on the exact asset pricing model. Equation (3) says that if you ran a regression of each stock’s excess returns on the aggregate risk factor:

, depends on the exact asset pricing model. Equation (3) says that if you ran a regression of each stock’s excess returns on the aggregate risk factor:

(4)

then the estimated intercept for each stock should be:

(5)

Thus, each stock’s average excess returns may well be related to its exposure to aggregate volatility since  shows up in the expression for

shows up in the expression for  ; however, idiosyncratic volatility,

; however, idiosyncratic volatility,  , better not be priced since it shows up nowhere above.

, better not be priced since it shows up nowhere above.

3. Aggregate Volatility

Ang, Hodrick, Xing, and Zhang (2006) show that stocks with more exposure to aggregate volatility have lower average excess returns. i.e., that the coefficient  . The authors actually look at each stock’s exposure to changes in aggregate volatility. To see how this changes the math, consider rewriting the intercept above as:

. The authors actually look at each stock’s exposure to changes in aggregate volatility. To see how this changes the math, consider rewriting the intercept above as:

(6)

Using this formulation, we can look at how perturbing  around its mean with some small

around its mean with some small  will impact the estimated intercept:

will impact the estimated intercept:

(7) ![\begin{align*} \mathrm{A}_n(\Delta \sigma_x) &= \mathrm{A}_n(0) + \mathrm{A}_n'(0) \cdot \Delta \sigma_x + \cdots \\ &\approx \left[ \alpha_n + \frac{\gamma_n}{2} \cdot \langle\sigma_x\rangle^2 \right] + \gamma_n \cdot \langle\sigma_x\rangle \cdot \Delta \sigma_x \end{align*}](https://alexchinco.com/wp-content/ql-cache/quicklatex.com-e4767386cedfa210b242c920cb810f29_l3.svg "Rendered by QuickLaTeX.com")

Since  by definition,

by definition,  and

and  will have the same sign. Thus, testing for whether exposure to changes in aggregate volatility is priced is tantamount to testing for whether exposure to aggregate volatility is priced.

will have the same sign. Thus, testing for whether exposure to changes in aggregate volatility is priced is tantamount to testing for whether exposure to aggregate volatility is priced.

The authors proceed in  steps. First, they calculate the changes in aggregate volatility time series using changes in the daily options implied volatility:

steps. First, they calculate the changes in aggregate volatility time series using changes in the daily options implied volatility:

(8) ![\begin{align*} \Delta \sigma_{x,d+1} = \mathit{VXO}_{d+1} - \mathit{VXO}_d \qquad \text{with} \qquad \mathrm{E}[\Delta \sigma_{x,d+1}] = 0.01{\scriptstyle \%}, \, \mathrm{StD}[\Delta \sigma_{x,d+1}] = 2.65{\scriptstyle \%} \end{align*}](https://alexchinco.com/wp-content/ql-cache/quicklatex.com-1fcb5273efb718f3d57f082e0e6e35a9_l3.svg "Rendered by QuickLaTeX.com")

If the VXO is  , then options markets expect the S&P 100 to move up or down over the next

, then options markets expect the S&P 100 to move up or down over the next  calendar days. The authors use the VXO contract price rather than the VIX contract price because it has a longer time series dating back to 1986. The only difference between the contracts is that the VXO quotes the options implied volatility on the S&P 100; whereas, the VIX quotes the options implied volatility on the S&P 500. Daily changes in the contract prices have a correlation of

calendar days. The authors use the VXO contract price rather than the VIX contract price because it has a longer time series dating back to 1986. The only difference between the contracts is that the VXO quotes the options implied volatility on the S&P 100; whereas, the VIX quotes the options implied volatility on the S&P 500. Daily changes in the contract prices have a correlation of  over the sample period from January 1986 to December 2012 as shown in the figure below.

over the sample period from January 1986 to December 2012 as shown in the figure below.

Second, the authors compute each stock’s exposure to changes in aggregate volatility by running a regression for each stock  using the daily data in month

using the daily data in month  :

:

(9)

Estimated coefficients are related to underlying deep parameters by:

(10)

The daily market excess return,  , is the excess return on the CRSP value-weighted market index. I include AMEX, NYSE, and NASDAQ stocks with

, is the excess return on the CRSP value-weighted market index. I include AMEX, NYSE, and NASDAQ stocks with  daily observations in month in my universe of

daily observations in month in my universe of  stocks.

stocks.

Third, the authors sort the stocks satisfying the data constraints in month into value-weighted portfolios based on their estimated  . Note that because the factor

. Note that because the factor  is common to all stocks in month , this sort effectively organizes stocks by their true exposure to aggregate volatility,

is common to all stocks in month , this sort effectively organizes stocks by their true exposure to aggregate volatility,  . For each portfolio

. For each portfolio  with

with  denoting the stocks with the lowest aggregate volatility exposure and

denoting the stocks with the lowest aggregate volatility exposure and  denoting the stocks with the highest aggregate volatility exposure, the authors then calculate the daily portfolio returns in month . The figure above shows the cumulative returns to each of these portfolios. It reads that if you invested

denoting the stocks with the highest aggregate volatility exposure, the authors then calculate the daily portfolio returns in month . The figure above shows the cumulative returns to each of these portfolios. It reads that if you invested  in the low aggregate volatility exposure portfolio in January 1986, then you would have over

in the low aggregate volatility exposure portfolio in January 1986, then you would have over  more dollars in December 2012 than if you had invested that same in the high aggregate volatility exposure portfolio. What’s more, each portfolio’s exposure to the excess return on the market is not explaining its performance. The figure below reports the estimated intercepts for each from the regression:

more dollars in December 2012 than if you had invested that same in the high aggregate volatility exposure portfolio. What’s more, each portfolio’s exposure to the excess return on the market is not explaining its performance. The figure below reports the estimated intercepts for each from the regression:

(11)

and indicates that abnormal returns are decreasing in the portfolio’s exposure to aggregate volatility.

Fourth, in order to test whether the spread in portfolio abnormal returns is actually explained by contemporaneous exposure to aggregate volatility, the authors then create an aggregate volatility factor mimicking portfolio. They estimate the regression below using the daily excess returns on each of the aggregate volatility exposure portfolios in each month :

(12)

and store the parameter estimates for  . They then define the factor mimicking portfolio return at daily horizon in month as:

. They then define the factor mimicking portfolio return at daily horizon in month as:

(13)

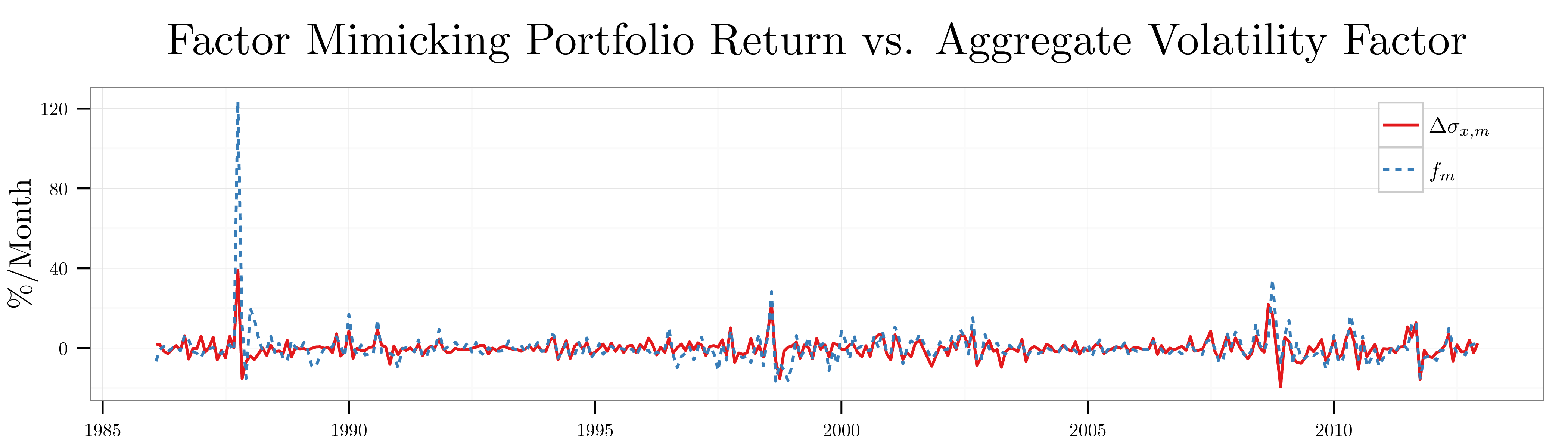

The figure below plots the factor mimicking portfolio returns against the underlying changes in aggregate volatility at the monthly level. The data series line up relatively closely; however, the factor mimicking portfolio is much too volatile during crises such as Black Monday in 1987.

Fifth and finally, the authors check whether or not each of the aggregate volatility portfolio’s returns are positively correlated with contemporaneous movements in the aggregate volatility factor mimicking portfolio at the monthly horizon. To do this, they cumulate up daily excess returns on the factor mimicking portfolio and the aggregate volatility exposure sorted portfolios to get monthly returns:

(14)

Then, they run the regression below at a monthly horizon over full sample:

(15)

I report the estimated  coefficients in the figure below. Consistent with the idea that exposure to aggregate volatility is driving the disparate excess returns of the test portfolios, I find that each portfolio loads positively on monthly movements in the factor mimicking portfolio.

coefficients in the figure below. Consistent with the idea that exposure to aggregate volatility is driving the disparate excess returns of the test portfolios, I find that each portfolio loads positively on monthly movements in the factor mimicking portfolio.

4. Idiosyncratic Volatility

Ang, Hodrick, Xing, and Zhang (2006) also show that stocks with more idiosyncratic volatility have lower average excess returns. This should not be true under the standard theory outlined in Section 2 above. To measure idiosyncratic volatility, the authors run the regression below at the daily level in month for each stock  :

:

(16)

where the risk factors are the excess return on the value weighted market portfolio, the excess return on a size portfolio, and the excess return on a value portfolio as dictated by Fama and French (1993):

(17)

For each stock listed on the AMEX, NYSE, or NASDAQ stock exchange with daily observations in month , the authors then calculate the measure of idiosyncratic volatility below:

(18) ![\begin{align*} \sigma_{z,n} &= \mathrm{StD}[\mathit{Error}_{n,d}] \end{align*}](https://alexchinco.com/wp-content/ql-cache/quicklatex.com-0e07c5257a89dc3d311fe765f3ef3663_l3.svg "Rendered by QuickLaTeX.com")

The authors sort the stocks satisfying the data constraints in month into value-weighted portfolios based on their estimated  values. The figure above reports the cumulative returns to these test portfolios. The figure reads that if you invested in the low idiosyncratic volatility portfolio in January 1963, then you would have over

values. The figure above reports the cumulative returns to these test portfolios. The figure reads that if you invested in the low idiosyncratic volatility portfolio in January 1963, then you would have over  more in December 2012 than if you had invested in the high idiosyncratic volatility portfolio. The figure below reports the estimated abnormal returns,

more in December 2012 than if you had invested in the high idiosyncratic volatility portfolio. The figure below reports the estimated abnormal returns,  , for each of the idiosyncratic volatility portfolios over the full sample and confirms that the poor performance of the high idiosyncratic volatility portfolio cannot be explained by exposure to common risk factors.

, for each of the idiosyncratic volatility portfolios over the full sample and confirms that the poor performance of the high idiosyncratic volatility portfolio cannot be explained by exposure to common risk factors.

5. Are They Related?

I conclude by discussing the obvious follow-up question: “Are these phenomena related?” After all, it could be the case that the firms with the highest exposure to aggregate return volatility also have the highest idiosyncratic volatility and vice versa. Ang, Hodrick, Xing, and Zhang (2006) show that this is not the case via a double sort. i.e., they show that within each aggregate volatility exposure portfolio, the stocks with the lowest idiosyncratic volatility outperform the stocks with the highest idiosyncratic volatility. Similarly, they show that within each idiosyncratic volatility portfolio, the stocks with the lowest aggregate volatility exposure outperform the stocks with the highest aggregate volatility exposure. Thus, the motivation driving investors to pay a premium for stocks with high aggregate volatility exposure is different from the motivation driving investors to pay a premium for stocks with high idiosyncratic volatility.

Indeed, you can pretty much guess this fact from the cumulative return plots in Sections and  where the red lines denoting the low exposure portfolios behave in completely different ways. e.g., the low aggregate volatility exposure portfolio returns behave more or less like the high aggregate volatility exposure portfolio returns but with a higher mean. By contrast, the low idiosyncratic volatility portfolio returns are a much different time series with dramatically less volatility. Interestingly, if the authors sort on total volatility in month rather than idiosyncratic volatility, then results are identical; however, the results to not carry through if you sort on

where the red lines denoting the low exposure portfolios behave in completely different ways. e.g., the low aggregate volatility exposure portfolio returns behave more or less like the high aggregate volatility exposure portfolio returns but with a higher mean. By contrast, the low idiosyncratic volatility portfolio returns are a much different time series with dramatically less volatility. Interestingly, if the authors sort on total volatility in month rather than idiosyncratic volatility, then results are identical; however, the results to not carry through if you sort on  in month . e.g., suppose you ran the same regression at the daily level in month for each stock :

in month . e.g., suppose you ran the same regression at the daily level in month for each stock :

(19)

where the risk factors are the excess return on the value weighted market portfolio, the excess return on a size portfolio, and the excess return on a value portfolio as dictated by Fama and French (1993):

(20)

Then, for each stock you computed the statistic measuring the fraction of the total variation in each stock’s excess returns that is explained by movements in the risk factors:

(21)

If you group stocks into portfolios based on their over the previous month, the figure above shows that there is no monotonic spread in the abnormal returns. Thus, the idiosyncratic volatility results seem to be more about volatility and less about the explanatory power of the Fama and French (1993) factors.

You must be logged in to post a comment.