1. Motivation

Kyle (1985) introduces an information-based asset-pricing model where informed traders keep trading until the marginal benefit of holding one additional share of the asset is exactly offset by the marginal cost of this last trade’s price impact. This model has really nice intuition, but it also has some undesirable features. For instance, traders in Kyle (1985) are risk neutral and don’t get to choose how much to learn about the asset. Grossman-Stiglitz (1980) gives an alternative model that addresses these two concerns but at the cost of dramatically changing the intuition of the model. In Grossman-Stiglitz (1980) all traders are price takers, meaning that informed traders don’t appreciate their own price impact. See my earlier post for more details.

In this post, I work through a simple model where all traders are risk averse and get to choose whether or not to learn about asset fundamentals and where the informed traders appreciate their own price impact.

2. Market Structure

Let’s consider a market with a one trading period and a single asset that pays out a liquidating dividend,  , at the end of the period. As is usually the case, this payout is normally distributed,

, at the end of the period. As is usually the case, this payout is normally distributed,

(1)

and has units of dollars per share. For simplicity, let’s set the net riskfree rate to  . In this market, there are

. In this market, there are  total traders, of which

total traders, of which  are informed while

are informed while  are uninformed. Let

are uninformed. Let  denote each informed trader’s demand for the asset in units of shares per trader and let

denote each informed trader’s demand for the asset in units of shares per trader and let  denote each uninformed trader’s demand in units of shares per trader. Thus, if there are

denote each uninformed trader’s demand in units of shares per trader. Thus, if there are  total shares of the asset available for purchase, then the market clearing condition is:

total shares of the asset available for purchase, then the market clearing condition is:

(2)

You can think about this random variation in asset supply in a few different ways. For instance, it might come from noise-trader demand or mechanical rebalancing decisions made by ETFs to name just two.

3. Informed Traders

Informed traders pay a cost,  , to learn the fundamental value of the asset, , prior to trading. These traders submit market orders, and, while they don’t know what the final market-clearing price will be, they do know that their own trading will impact the price. Thus, they choose their demand, , in order to maximize their utility,

, to learn the fundamental value of the asset, , prior to trading. These traders submit market orders, and, while they don’t know what the final market-clearing price will be, they do know that their own trading will impact the price. Thus, they choose their demand, , in order to maximize their utility,

(3) ![\begin{align*} - \, \mathrm{E}\left( \, e^{- \phi \cdot [ \, (\hat{v} - p) \cdot x_i - \lambda \, ]} \, \middle| \, \hat{v} \, \right), \end{align*}](https://alexchinco.com/wp-content/ql-cache/quicklatex.com-a1b7cf7f29360a162ebd8e0868b7d9e4_l3.svg "Rendered by QuickLaTeX.com")

where  is their risk-aversion parameter in units of traders per dollar. Let’s guess that each informed trader’s demand rule is linear in the fundamental asset value,

is their risk-aversion parameter in units of traders per dollar. Let’s guess that each informed trader’s demand rule is linear in the fundamental asset value,

(4)

where  has units of shares per trader and

has units of shares per trader and  has units of squared shares per dollar per trader. It’s possible to verify later that this linear symmetric demand rule for the informed traders is indeed optimal.

has units of squared shares per dollar per trader. It’s possible to verify later that this linear symmetric demand rule for the informed traders is indeed optimal.

4. Uninformed Traders

In contrast to the informed traders who see the fundamental asset value but not the price, the uninformed traders see price but not fundamental asset value. Select menu of price-quantity pairs,  , that they’d be willing to trade—just like in Grossman-Stiglitz (1980). They choose this menu in order to maximize their utility,

, that they’d be willing to trade—just like in Grossman-Stiglitz (1980). They choose this menu in order to maximize their utility,

(5)

where is their risk-aversion parameter in units of traders per dollar. Because the uninformed traders don’t do any research to uncover the fundamental value of the asset, they don’t pay any learning costs, . The uninformed traders’ first-order condition characterizes how many shares they are willing to buy at each price:

(6)

The market then clears via a menu auction. Informed traders submit their market orders and uninformed traders submit their menu of acceptable price-quantity pairs, and then an auctioneer sells each share at the market-clearing price.

5. Price Signal

The key to solving the model is understanding how informative this market-clearing price is for the uninformed traders. To do this, let’s guess that the pricing rule is linear,

(7)

where  has units of dollars per share,

has units of dollars per share,  is dimensionless, and

is dimensionless, and  has units of dollars per squared share. If the pricing rule is indeed linear—and, it’s easy to see that this is the case after solving model—then this means price gives unbiased signal about the fundamental value of the asset,

has units of dollars per squared share. If the pricing rule is indeed linear—and, it’s easy to see that this is the case after solving model—then this means price gives unbiased signal about the fundamental value of the asset,

(8)

with variance  . Thus, conditional on observing the market-clearing price, uninformed traders have posterior beliefs about the fundamental value of the asset,

. Thus, conditional on observing the market-clearing price, uninformed traders have posterior beliefs about the fundamental value of the asset,

(9) ![\begin{align*} \begin{matrix} \mathrm{Var}(\hat{v}|p) = (1 - \kappa) \times \sigma_v^2 & \quad \text{and} \quad & \mathrm{E}(\hat{v}|p) = \kappa \times \sfrac{1}{\beta_1} \cdot (p - [\beta_0 - \beta_2 \cdot \mu_s]), \end{matrix} \end{align*}](https://alexchinco.com/wp-content/ql-cache/quicklatex.com-554081e7dc7fe1c0b86ee183c641a91b_l3.svg "Rendered by QuickLaTeX.com")

where  is a dimensionless constant.

is a dimensionless constant.

6. Market Clearing

Market clearing implies that the total demand from the informed traders and the total demand from the uninformed traders is exactly equal to the aggregate supply of the asset:

(10)

If we plug in the expressions for the uninformed traders’ beliefs about the mean and variance of the asset value given the price, then we can rearrange this equation to get a pricing rule:

(11)

Matching coefficients then gives us the following equations characterizing the equilibrium pricing rule:

(12)

7. Optimal Demand

Given this pricing rule, what’s an informed trader to do? To answer this question, first notice that we can rewrite the pricing rule as follows,

(13)

so that the equilibrium price is a constant term,  , plus a response to the aggregate demand,

, plus a response to the aggregate demand,  . If we plug this formula for the price into the

. If we plug this formula for the price into the  th informed trader’s optimization problem,

th informed trader’s optimization problem,

(14)

then taking the first-order condition yields the following expression for his optimal demand rule,

(15)

Thus, for any number of informed and uninformed traders, and , we are left with a system of  equations and unknowns characterizing the equilibrium values for , , , and

equations and unknowns characterizing the equilibrium values for , , , and  after noticing that

after noticing that  . With these values in hand, we can also solve for , , and . All that is left to do is figure out how many traders will choose to learn about the fundamental value of the asset at a cost of .

. With these values in hand, we can also solve for , , and . All that is left to do is figure out how many traders will choose to learn about the fundamental value of the asset at a cost of .

8. Learning Choice

Each trader makes his decision about whether to become informed prior to trading. Thus, in equilibrium, no trader should want to unilaterally change his learning choice:

(16)

No informed trader should regret learning the fundamental value of the asset and no uninformed trader should regret not learning it. If we plug in the functional forms for the pricing rule and the informed-trader demand rule into an informed trader’s utility function, we get the following quadratic form:

(17)

Thus, if we write  , we can characterize each informed trader’s unconditional expectation of his utility as,

, we can characterize each informed trader’s unconditional expectation of his utility as,

(18)

where the constants  ,

,  , and

, and  are given by:

are given by:

(19)

Applying the same tricks to an uninformed trader’s utility function gives the following quadratic expression,

(20)

with analogous constants:

(21)

Equating the two unconditional expectations pins down the number of informed traders in equilibrium.

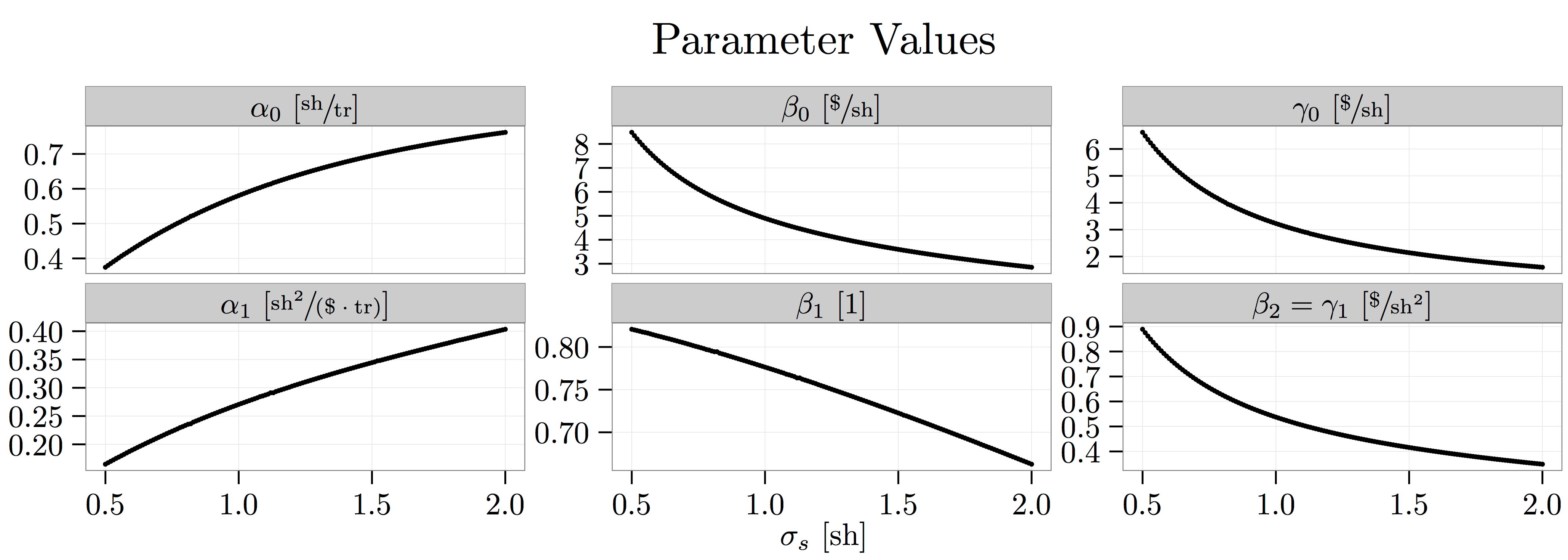

9. Equilibrium Analysis

Let’s wrap up this post by looking at how the equilibrium changes as we vary the amount of noise-trader demand volatility,  . In all of the plots below, I use the following parameterization:

. In all of the plots below, I use the following parameterization:  ,

,  ,

,  ,

,  , and

, and  . You can find the code used to create these plots here.

. You can find the code used to create these plots here.

You must be logged in to post a comment.